F Test on seasonal dummies

We use the GLS \(F^{M}\) -statistic of Lytras, Feldpausch and Bell (2007). It requires defining stable or fixed seasonal regressors, \(M_{j,t}\). For monthy data each one of the 11 regressors required is defined as follows:

\[M_{j,t}=\left\{ \begin{matrix} 1 &\;& in \; month \; j=1,...,11 \\ -1 &\;& in \; December \\ 0 &\;& otherwise\\ \end{matrix} \right\}\]Those regressors would enter in a regARIMA model, resulting on the following general expression:

\[\left( 1 - B \right)^{d}(Y_{t} - \beta_1 M_{1,t} - \ldots - \beta_{11} M_{11,t} - \gamma X_{t}) = \left( 1 + L \right)\alpha_t\]One can use the individual t-statistics to assess whether seasonality for a given month is significant, or a chi-squared test statistic if the null hypothesis is

that the parameters are collectively all zero. The chi-squared test statistic

\(\hat{\chi}^2 = \hat{\beta}^{'}[Var(\hat{\beta})]^{-1}\hat{\beta}\)

is in this case compared to critical values from chi-squared distribution with 11 degrees of freedom.

Since \(Var(\hat{\beta})\) is computed using the estimated variance of \(\alpha_t\) may be actual variance in small samples, this test is corrected using the proposed \(F^{M}\) -statistic:

\[F^{M}= \frac{\hat{\chi}^2}{11} \times \frac{n-d-k}{n-d}\]where \(n\) is the sample size, \(d\) is the degree of differencing and \(k\) is the total number of regressors in the regARIMA model (including 11 seasonal dummies \(M_{j,t}\) and the intercept). This statistic follows a \(F_{11,n-d-k}\) distribution under the null.

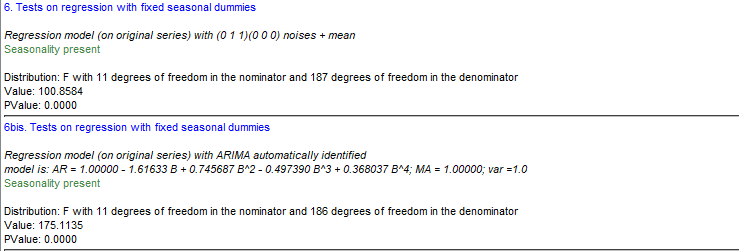

Example of how results are displayed:

References

Lytras, D. P., Feldpausch, R. M., and Bell, W. R. (2007), “Determining Seasonality: A Comparison of Diagnostics from X-12-ARIMA,” Proceedings of the Third International Conference on Establishment Surveys, Montreal, Canada